More Australians are exploring specialist lending options. One area that continues to grow in popularity is using a self-managed super fund (SMSF) to purchase property.

With SMSF funds now accounting for over $27 billion in loans, (specifically, through limited recourse borrowing arrangements or LRBAs) the market is prime for growth, as trustees look to refinance mid-term loans to optimise their portfolio and younger SMSF trustees look to break into this market.

The opportunity behind SMSF lending

More Australians are choosing self-managed super funds to take a hands-on approach to their retirement savings. For many, property stands out as a popular investment option within that structure.

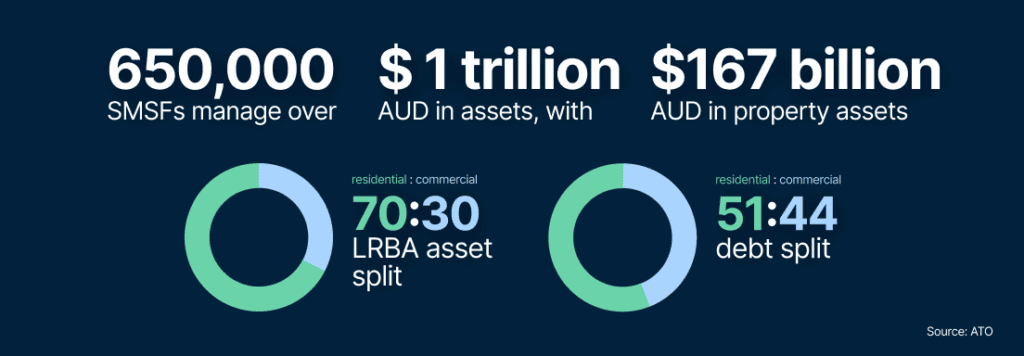

According to the Australian Taxation Office (ATO), SMSFs collectively manage over $1 trillion in assets, with $161bn of residential and non-residential property. In addition to this, there is $70 billion of property assets secured by limited recourse borrowing arrangements (LRBAs), which is when the SMSF trustee takes out a loan to purchase property though a SMSF. This reflects a growing appetite among trustees to diversify their portfolios with tangible assets that align with long-term retirement goals.

The state of SMSF property investment in Australia

Aussies have been able to invest in property through their SMSF for 18 years now. As of 2025, assets are split roughly 50:50 between residential and commercial property, however when we go deeper and look at the value split, it leans 70:30 towards commercial, due to the higher values of commercial property.

In fact, the rise of SMSF lending is only growing amongst younger generations “Since mandatory super contributions were introduced in 1992, we’re seeing Gen X and Millennials having a more sizeable super balance at an earlier age compared to previous generations, as it’s been a forced savings for most their working life,” says Richard Chesworth, our head of specialised distribution.

What SMSF investors should lookout for

According to Chesworth, “Key areas we’re seeing issues arise when SMSF trustees acquire the property in the wrong entity, as they sign a contract in the SMSF trustees name, however the SMSF only acquires beneficial ownership and contracts should be executed in the bare trustee name,”

Knowing your options and obligations as a SMSF trustee is key. While big banks usually focus on standard income and cookie-cutter profiles, when it comes to SMSF loans that need a bit more flexibility, a non-bank lender like Bluestone could be a unique fit for trustees with complex, irregular or unique income situations. Importantly, talk to your financial adviser, accountant and mortgage broker if you’re considering an SMSF or taking the next step to borrow and acquire property to ensure it’s aligned with your retirement needs.

How Bluestone supports more borrowers

Bluestone has been supporting property investors and their brokers with a unique approach that’s built around flexible lending options. We’re with you and your broker every step of the way.

If you’re considering property investment, speak to your broker and financial adviser to explore your options and understand what solutions are available for your situation.

The information provided in this article is general in nature and is not intended to be financial advice.

{kind=link}